Pillar 3a in the Corona year: one in five invested less

Wage losses due to short-time work or redundancies put pressure on the savings rate of many Swiss people in the Corona year. According to a survey by Comparis, over 20 percent of 3a savers invested less or not at all in voluntary tied pension provision in 2020.

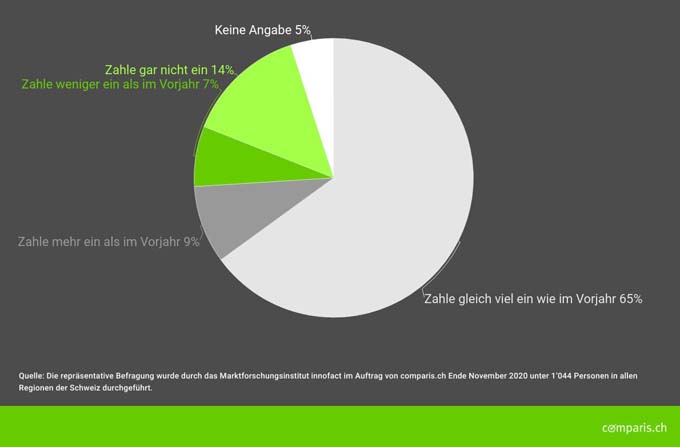

In a representative survey conducted at the end of November by the online comparison service Comparis, 53 percent of survey participants said they had a 3a pension solution. Of these, almost one in five (21 percent) paid less or not at all into the third pillar in the past year. "This reflects, among other things, the loss of wages due to short-time work as well as Corona-related layoffs," says Leo Hug, pension expert at Comparis. When asked about the reasons for not paying in, 43 percent of those affected claimed a lower income than in the previous year.

36 percent have invested savings portion elsewhere in 2020

Although income setbacks are the most frequently cited argument for declining transfers to pillar 3a, they are not the only one. 19 percent of 3a savers who paid less or nothing into their retirement savings account said they had used their savings portion for other investment vehicles, such as direct investments in equities in a bank custody account. 17 percent of respondents said they had no money left over for the third pillar because of a major purchase.

Three quarters of people who normally pay into pillar 3a invested the same amount of money or more in tax-privileged private pension provision in 2020 than in the previous year. Of these, slightly more than half (59 percent) paid in the maximum amount (CHF 6,826 for people with a connection to a pension fund) - significantly more men than women (64 percent versus 52 percent).

Early retirements have an effect on pillar 3a

80 percent of 3a savers aged up to 55 invested more or the same amount in pillar 3a last year as in the previous year. By contrast, only 56 percent of those over 56 did so. A quarter (25 percent) of those over 56 even decided not to pay into their 3a account at all.

"The significantly lower payments of the elderly are hardly related to economic consequences of the Corona pandemic," Hug explains. "In this age group, there are many early retirees without earned income subject to AHV who have not yet cashed out their pillar 3a."

Source: Comparis