Is a global economic crisis looming? An assessment.

Politicians are trying to slow down the spread of the Corona pandemic with extraordinary measures. That is right, because the health of the population has absolute priority. But we are also interested in the question of what this means for the global economy. Are the last few weeks the beginning of a global economic crisis, or will everything settle down on the economic front in a few months? A classification by hpo forecasting on the current development of the global economy.

From an economic perspective, the question of the hour is what the consequences of this pandemic will be for companies. As with the SARS epidemic in 2003, can we expect a brief economic slump that will then be corrected very quickly? Or will it end in a full-blown economic crisis this time? We explore this question in this economic commentary by hpo to get to the bottom of the current situation.

The factual situation before the coronavirus

In order to be able to make an assessment of the future, it is first necessary to take stock of the facts. In our real economic model, we focus on industrial production, consumption and sentiment indicators. In particular, we are interested in how the situation looked before we all fell under the spell of the corona virus:

- Industrial production: Demand for capital goods already weakened in 2019 in Europe, Asia and most recently also in the USA. Compared with 2018, order intake for mechanical engineering companies in Germany fell by 9 %, for example. Although the figures for order intake in the first two months of 2020 are not yet available, many industrial companies are already reporting a renewed sharp drop in order intake figures in some cases since the beginning of the year.

- Consumption: Consumption growth rates in Asia have been leveling off for some time and are well below the long-term trend growth. In Europe and North America, consumption was still very strong as of the end of 2019, but the momentum here also showed a sideways movement during this period. The hpo forecasting model has been indicating for some time that a substantial deterioration in consumer sentiment is also to be expected in the West in 2020. With the rapid spread of the coronavirus and the measures adopted by governments, this has now occurred even more rapidly and much more violently than expected. Even though there are still no reliable figures, it is clear that the shutdown of entire regions and countries means that a sharp decline must be expected.

- Sentiment indicators for industry (e.g. the OECD's Business Confidence Index or the Purchasing Managers Index Industry) have in the past been very reliable indicators of the development of demand in the capital goods industry. In recent months, these indicators have moved clearly into contractionary territory in most major markets, pointing to a downturn - again independently of the corona virus. Initial sentiment indicators from China at the beginning of 2020 suggest a dramatic slump there; reliable figures for the world regions are yet to come.

Harbingers of a global economic crisis

The following interim conclusion can be drawn: The global economy was already in an unstable phase before the outbreak of the corona virus. With hpo forecasting's forecast models, we observe and analyze around 100 sub-sectors of the capital goods industry worldwide. These indicated early on - independently of the coronavirus - an accelerating decline in order intake in the capital goods industry for 2020 in almost all sectors. Also, hpo forecasting's Peter Meier forecast model has long indicated a slump in consumption in Europe and the U.S. for 2019/2020, similar to what was already observable in Asia. Our previous estimates for 2020 are not only consistent in our quarterly economic commentariesbut also in an article of the Neue Zürcher Zeitung from May 14, 2018, in an interview in the Technical Review July 2019 as well as in a contribution of the Business magazine ECO on Swiss television from August 26, 2019 well documented.

Coronavirus is the trigger but not the cause of the looming economic crisis

There is now a very high probability that the coronavirus is the trigger for a downturn in the global economy. According to our analyses, the fundamentals of the real economy have been pointing to an economic crisis for some time. However, until now it was completely unclear what the trigger would be. Every global economic crisis can be linked to a major event. In the structural crisis of the 1990s, this was the disintegration of the Eastern bloc and the war in Iraq. The 2001 downturn is strongly associated with the bursting of the dotcom bubble and the September 9 terrorist attacks in the United States. And in the 2008 financial crisis, images of freshly laid-off investment bankers on the sidewalks of New York and London with cardboard boxes in their arms are etched in our collective memory. What all these economic crises have in common is that, long before the particular trigger was known, the economy was moving toward a period of instability.

The same is now true of the current downturn. The current economic crisis - of which we are only seeing the beginning at the moment - could also have been triggered by any other event. Our secret favorites so far have been the U.S. trade wars, an escalation in Iran, a hard BREXIT, the U.S. repo crisis or the unrest in Hong Kong. However, it became apparent once again that the trigger is usually an event that no one expects. Even if, according to epidemiologists, it had long been clear that a pandemic was possible at any time, the spread of this virus - and the violent reactions of governments to it - could not have been predicted, at least in terms of the specific timing. However, it was possible to recognize the unstable situation of the global economy on the basis of real economic indicators. From an economic point of view, we now have the misfortune that COVID-19 enters our lives precisely in this economically unstable phase, when consumption and investment cycles have just passed their peaks.

Cyclic instability

When the consumption and investment cycles have passed their peaks, the economy is unstable. In the past, this happened every seven to twelve years. Then all it took was a random trigger to cause the crisis to erupt. In fact, at least in terms of consumption in Asia and in early-cycle sectors of the capital goods industry, the crisis already began about a year ago. Nevertheless, there is a high probability that the current downturn will go down in the history books as the Corona crisis.

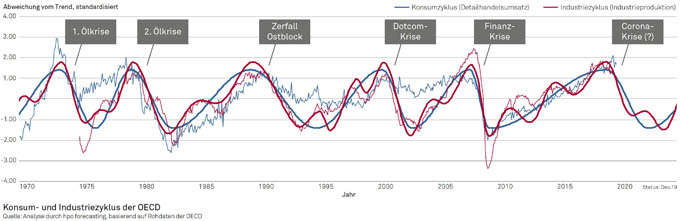

The chart below shows the deviation from the long-term trend of retail trade and industrial production in the OECD. The effective values can be approximated with sine curves of different wavelengths. The values from 2020 onwards show the hypothetical trend for the future and were created before the outbreak of the Corona epidemic. Whenever the consumption and investment cycles peaked, they were followed by a global economic crisis. With the help of the Peter Meier forecasting model from hpo forecasting, the cycles can be reliably forecast. Thus, it was possible for Peter Meier to predict the dotcom crisis of 2001, the financial crisis of 2008 and also the current downturn with a lead time of about two years. Further details on this model can be found in Peter Meier's book "Die Wirtschaft als schwingendes System" (Hanser Verlag, 2019).

Where do we go from here?

Due to the economically unstable phase described above in combination with the severe Corona shock, a global economic crisis is likely. However, this can have very different effects on different industries and sub-industries. We analyze these global effects in our daily work. With the help of industry models, we are also able to produce reliable forecasts of order intake for individual companies.

A major factor of uncertainty is the reaction of politicians and the financial markets. In view of the extraordinary situation, it is appropriate to take drastic measures to protect the population and thus slow down the spread of the virus.

Overloading of healthcare providers must be kept to a minimum, because people's health is the top priority. However, the sometimes drastic effects of the measures already taken on the economy cannot be denied. The more drastic these measures, the greater the short-term economic impact. In the medium and long term, however, real economic cycles are likely to remain the dominant factors - at least for the capital goods industry. The problem now is that these cycles - irrespective of COVID-19 - also point to a negative trend. The sectors of the economy already severely affected by the decline in the real economy are currently being further impacted by the pandemic.

We see a major risk in the high level of corporate debt worldwide. For many highly indebted companies, several months of poor business performance are enough for them to get into financial difficulties and no longer be able to service their liabilities despite low interest rates. If this happens on a large scale, the outlook is likely to deteriorate further and, in an extreme case, a financial crisis will occur in the next few quarters.

There are also bright spots

However, companies that have a solid balance sheet and are therefore able to weather a drastic downturn may well emerge stronger from a crisis. This is because some competitors will exit the market for financial reasons. Particularly in the fragmented mechanical engineering sector, there may be favorable opportunities for takeovers. Furthermore, substitution effects can already be observed anecdotally in individual sub-sectors, for example when Western companies replace their Chinese suppliers with European suppliers.

Conclusion: Initial situation for a global economic crisis is given

The starting point for a global economic crisis has clearly intensified. This coincides with the economic outlook presented by hpo forecasting at a time when we still associated Corona primarily with Mexican beer. Due to recent events, we now also know with a high degree of probability the trigger of the crisis.

However, the outbreak has hardly any major impact on our medium- and long-term forecasts, which were already pessimistic. The consequences of the global downturn for the individual sectors and subsectors must be analyzed on the basis of the differentiated sector models.

Authors:

Joshua Burkart, M. A. HSG, is Managing Director at hpo forecasting. Benjamin Boksberger, M. A. HSG, is Senior Consultant ebenda. The forecasting specialists at hpo forecasting prepare company-specific forecasts of incoming orders for industrial companies. The forecasts are based on the scientifically founded and empirically proven Peter Meier forecasting model.